The link with ESG criteria

December and Santa’s ESG blunders are long gone – and after a few changes, investors have returned and Santa Inc.’s stocks have soared.

In case you don’t understand the connection, we wrote in December about the influence investors can exert by buying the shares of companies that take into account ESG criteria – ESG stands for environmental, social, and governance.

Today, we’re looking at the environmental aspect: how can companies measure their environmental impact, and how can they communicate it to stakeholders?

What is being measured?

Conversations about environmental challenges often focus on climate change.

As the IPCC acknowledged in its latest report, global warming is caused by human activity. It can therefore only be slowed down or stopped by adapting our production and consumption habits.

That means, among others, a little less nuggets and a little more green beans on our plates.

Climate change is particularly linked to the greenhouse effect, which human activities have disrupted through their excessive emissions of gases (known as “greenhouse gases”), including carbon dioxide (CO2), methane (CH4) and many others.

The 3 scopes: a reporting framework

To make organizations, which are the source of a large part of our emissions, accountable, the Greenhouse Gas Protocol (GHG Protocol) was set up in the late 1990s by the World Resource Institute and the Word Business Council for Sustainable Development, with the help of governments, companies and NGOs.

To address a global challenge, it is easier to speak the same language.

Thus, in 2001, the first standard for accounting and reporting of GHGs (greenhouse gases) was published, providing a common reporting framework for companies.

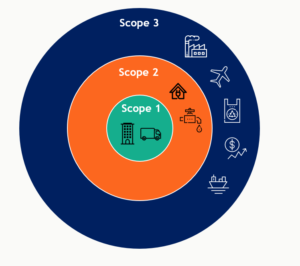

This standard has three scopes that focus on the different sources of emissions produced by companies. They are called scopes 1, 2 and 3.

- Scope 1 measures direct emissions from the combustion of fossil fuels of company-owned (or controlled) resources. This includes, for example, emissions from your cows, fumes from your industrial ovens, etc.

- Scope 2 measures indirect emissions related to the purchase or production of electricity. For example, electricity produced by a third party and consumed by your company to print magazines or run your servers.

- Scope 3 measures all other indirect emissions from the extended value chain – upstream and downstream – which often account for the majority of emissions. For example, a company that buys steel from a supplier will include the emissions related to that purchased steel in its reporting.

Overview of the scopes and emissions of the value chain according to the GHG Protocol.

Source : ghgprotocol.org

How does it work?

Now that we know how to categorize our measures… how do we actually measure them?

A round of applause for the Carbon Balance Method developed for ADEME by Jean-Marc Jancovici.

This method defines direct and indirect GHG (greenhouse gas) emissions in carbon dioxide equivalent (CO2e) over a year.

When possible, we first try to estimate GHG emissions using physical ratios: we multiply the quantity consumed (kilometer traveled, liter of gasoline, kilogram of meat, surface in square meters) by the unit quantity of CO2 emitted.

For example, taking the TGV emits 1.73 gCO2e per passenger (= unit quantity, the passenger), per kilometer (= quantity consumed). So on a trip from Paris to Marseille of 750 km that would be 1298 gCO2e, or more than 1kg of CO2e.

When physical data are missing, a monetary ratio is used, expressed in CO2e per euro or dollar spent, to estimate the carbon footprint of a product or service from its purchase price. This method is often simpler to implement for scope 3, but less accurate than the physical data approach.

For example, a pharmaceutical company purchasing $1,000 worth of paper packaging will have to take into account the emission of 1.8 tons of CO2.

Sounds complicated? Don’t worry!

Most large companies rely on internal experts or specialized service providers to determine their carbon footprint.

In France, an annual carbon assessment is mandatory for all companies with more than 500 employees, since the Grenelle 2 law was passed in 2010 and must be updated at least every 4 years.

However, this law limits the obligation to scopes 1 and 2, whereas scope 3 is known to be the most significant in terms of GHG emissions…

Including scope 3 in the reporting requirements would therefore mean a major step towards a more realistic representation of companies’ carbon footprint.

System limitations

Some of you may say “emissions are not the only problem”, and you would be right.

But let’s be clear: the GHG protocol and its 3 scopes are not intended to address all aspects of sustainable development. Rather, it aims to provide a clear and quantified overview of the impact of companies on global warming.

For each sustainable development area, there are relevant indices. So how can we get a global view of our environmental performance? More and more companies are turning to environmental rating agencies such as CDP, MSCI or Ecovadis. Another exciting topic that we will talk about next time.

To help companies address the issue of sustainability, we have developed a training program, also available in English. It deals with the business opportunities of a sustainable company, ways to facilitate the transition, as well as opportunities to become actors of change.

Let’s talk about it over coffee?